Accounting

American Institute of Certified Public Accountants (AICPA) which defines accounting as “the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events, which are, in part at least, of a financial character and interpreting the results thereof”. It is the process of identifying, measuring & communicating the economic information of an organisation to its users who need the information for decision making.

Objectives of Accounting

It may differ from business to business depending upon their specific requirements. However, the following are the general objectives of accounting:

1.To ascertain the results of the operation:

2.To ascertain the financial position of the business:

3.To portray the liquidity position:

4.To protect business properties:

5.To facilitate rational decision – making:

6.To keeping systematic record:

7.To satisfy the requirements of law

BRANCHES OF ACCOUNTING

The changing business scenario over the centuries gave rise to specialized branches of accounting which could cater to the changing requirements. The branches of accounting are:

i) Financial accounting;

ii) Cost accounting; and

iii) Management accounting.

1. Financial Accounting

The accounting system concerned only with the financial state of affairs and financial results of operations is known as Financial Accounting. It is the original form of accounting. It is mainly concerned with the preparation of financial statements for the use of outsiders like creditors, debenture holders, investors and financial institutions. The financial statements i.e., the profit and loss account and the balance sheet, show them the manner in which operations of the business have been conducted during a specified period.

2. Cost Accounting

In view of the limitations of financial accounting in respect of information relating to the cost of individual products, cost accounting was developed. It is that branch of accounting which is concerned with the accumulation and assignment of historical costs to units of product and department, primarily for the purpose of valuation of stock and measurement of profits. Cost accounting seeks to ascertain the cost of unit produced and sold or the services rendered by the business unit with a view to exercising control over these costs to assess profitability and efficiency of the enterprise. It generally relates to the future and involves an estimation of future costs to be incurred. The process of cost accounting based on the data provided by the financial accounting.

3. Management Accounting:

It is an accounting for the management i.e., accounting which provides necessary information to the management for discharging its functions. According to the Anglo-American Council on productivity, “Management accounting is the presentation of accounting information is such a way as to assist management in the creation of policy and the day-to-day operation of an undertaking.” It covers all arrangements and combinations or adjustments of the orthodox information to provide the Chief Executive with the information from which he can control the business e.g. Information about funds, costs, profits etc. Management accounting is not only confined to the area of cost accounting but also covers other areas (such as capital expenditure decisions, capital structure decisions, and dividend decisions) as well.

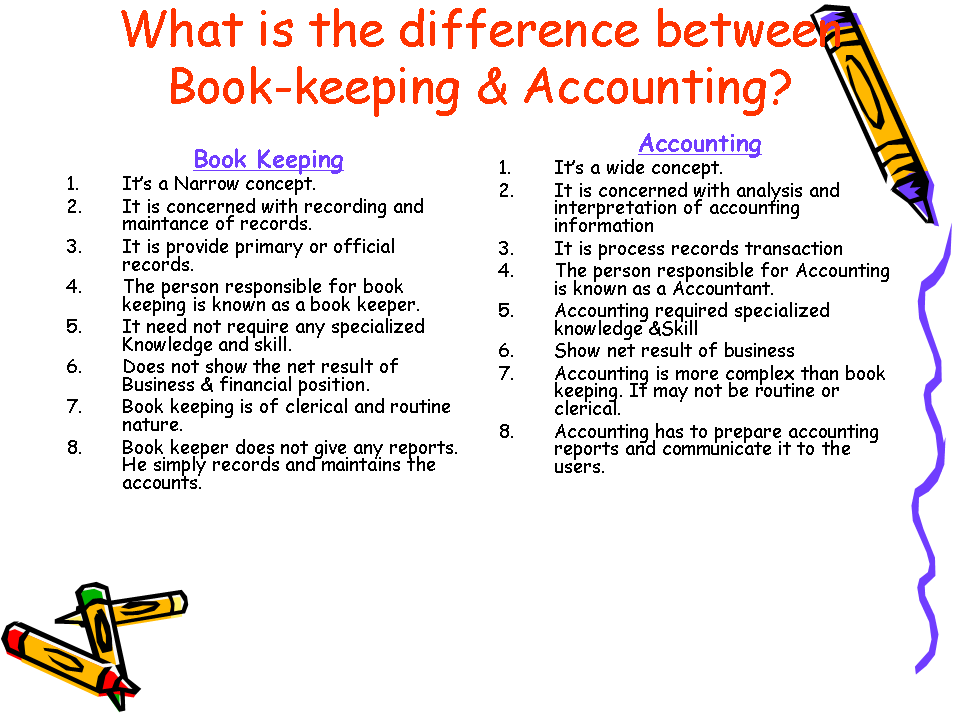

Accountancy, Accounting, & Book-keeping

Accountancy refers to a systematic knowledge of accounting.

Accounting refers to the actual process of preparing and presenting the accounts.

Book-keeping is a part of accounting and is concerned with record keeping or maintenance of books accounting which is often routine and clerical in nature.

Users of Accounting information & their needs

1.Short term creditors

2.Long term creditors

3.Present investors

4.Potential investors

5.Management

6.Employees

7.Tax authorities

8.CustomerKey Notes :- Basics of Accounting

No comments:

Post a Comment